Welcome

DIY BRANDABLE CAMPAIGNS

Everything you need to create your own marketing campaigns using our brandable templates and campaign assets. To get started, click the asset you would like to use below. Highlight and right-click the text, select Copy, and then paste the text into your website, email, or social media sites.

CAMPAIGN ASSETS

Can you spend the same dollar twice? The answer, of course, is no. Yet, many clients may mistakenly believe otherwise when presented with Indexed Universal Life (IUL) illustrations designed with a “Swiss Army Knife” approach. These illustrations typically show the maximum possible income level, assuming participating loans. While this is not inherently problematic, it becomes a concern when living benefit features play a significant role in the sales strategy.

Understanding the Client’s Perspective

Most clients are drawn to the appeal of a single financial product that offers death benefit protection, supplemental retirement income, and a safety net for long-term care. However, unless advisors take the time to clarify policy mechanics, clients may assume these benefits are independent rather than sourced from the same pool of funds. This misunderstanding often leads to an expectation that living benefits, such as a Chronic Illness or Long-Term Care Accelerated Benefit Rider (ABR), are additional to any income withdrawn from the policy. The reality, however, is quite different: utilizing policy loans for income can significantly limit access to these living benefits.

The Loan Repayment Factor

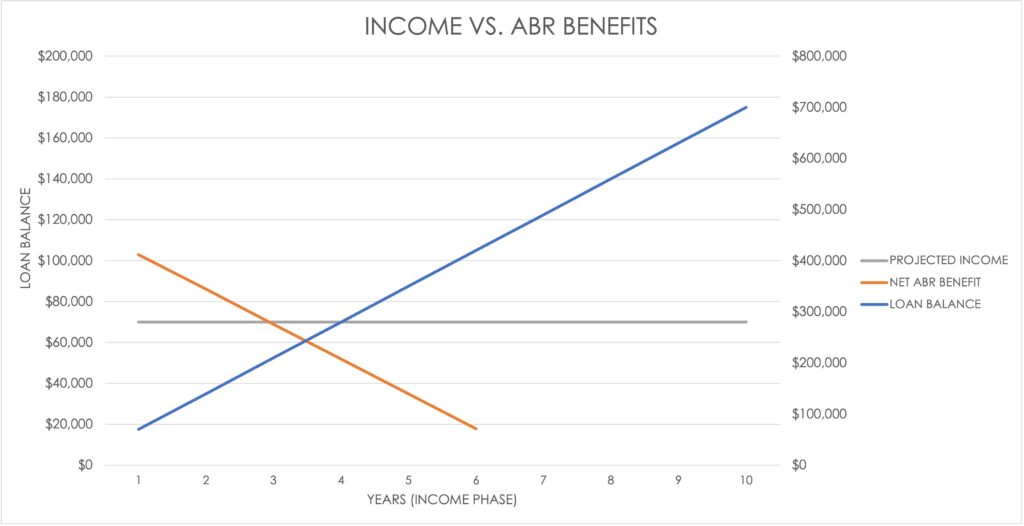

A key factor contributing to this issue is the structure of most ABRs, which typically require partial repayment of any outstanding loans with each benefit payment. Even a modest loan balance can lead to a net benefit lower than the client’s income. Additionally, many ABRs prohibit taking loans and ABR benefits in the same year. Figure 1 below illustrates how quickly an outstanding loan balance can erode the net benefit from the ABR, often reducing it below the policyholder’s expected income within just a few years.

Figure 1: Impact of Loan Balances on ABR Net Benefits

Strategic Solutions

Advisors can help clients navigate these complexities by adjusting how income is illustrated and withdrawn from the policy. Implementing the following best practices can enhance policy sustainability and benefit accessibility:

- Illustrate Income via Withdrawals First – Rather than relying on loans from the outset, structure income withdrawals to come from the policy’s basis first. This delays the accumulation of loan balances that would later need repayment.

- Delay Income Start Date – Pushing income withdrawals to a later age helps preserve meaningful ABR benefits and minimizes loan balance growth.

- Optimize Claim Timing – Rather than immediately filing an ABR claim when care is needed, consider increasing loan-based withdrawals for a projected five-year period. This often results in a larger net benefit than immediate ABR activation, while reducing administrative burdens and delays associated with claims processing.

The Case for a Multi-Policy Approach

While these strategies mitigate risk, they do not eliminate the fundamental issue that all benefits originate from the same policy pool. For clients who genuinely seek comprehensive protection—death benefits, retirement income, and long-term care—a multi-policy solution is often superior. However, this approach requires a higher financial commitment, which may not be feasible for all clients. In such cases, a well-structured and properly managed single-policy strategy remains a viable alternative.

By proactively educating clients on these nuances and employing thoughtful case design, individuals can maximize their IUL policies while avoiding unexpected limitations on benefits.

Many clients believe IUL is the ultimate financial Swiss Army knife—offering death benefits, supplemental income, and living benefits without compromise. But are they seeing the full picture?

The Hidden Trade-Offs

Illustrations often show max income potential through participating loans. However, clients may not realize that:

- Living benefits (like Chronic Illness & LTC riders) pull from the same pool as income.

- Loan balances can erode Arbor Realty Trust (ABR) payouts, sometimes reducing benefits below expected income.

- Some policies prohibit loans & ABR benefits in the same year.

Smart Solutions for Advisors

- Illustrate income through withdrawals first.

- Delay income start dates to preserve benefit access.

- Consider a multi-policy approach for true protection.

The key? Educate clients early to prevent unpleasant surprises.

Advisors, how do you navigate these IUL pitfalls in your practice? Drop your insights below!

#InsuranceAdvisors #IUL #FinancialPlanning #LifeInsurance #RetirementIncome #WealthProtection #LongTermCare

Subject Line: Avoid Costly IUL Pitfalls – Here’s How

Too often, clients believe they can maximize income and access living benefits without trade-offs. But as you know, policy loans can significantly reduce—or even eliminate—expected benefits from Chronic Illness or Long-Term Care riders.

The good news? With the right case design, you can help clients avoid these pitfalls. Strategies like illustrating withdrawals first, delaying income start dates, and considering a multi-policy approach can make all the difference.

Let’s schedule a quick call to discuss how you’re structuring IUL solutions for your clients.

Best,

[Your Name and Contact Information]

Insurance Beyond Protection.

CONTACT

© Brokerage Solutions. All Rights Reserved.

Securities offered through The Leaders Group, Inc., Member FINRA/SIPC, 475 Springfield Ave., Summit, NJ 07901, (303) 797-9080. Brokerage Solutions, LLC is not affiliated with The Leaders Group, Inc.