Welcome

DIY BRANDABLE CAMPAIGNS

Everything you need to create your own marketing campaigns using our brandable templates and campaign assets. To get started, click the asset you would like to use below. Highlight and right-click the text, select Copy, and then paste the text into your website, email, or social media sites.

CAMPAIGN ASSETS

The Smartest Way to Fund a Buy-Sell Agreement: Unlocking Financial Security for Business Owners

As financial advisors, guiding business owners through the complexities of succession planning is a critical responsibility. One of the most effective tools in this process is a well-structured Buy-Sell Agreement (BSA), which ensures business continuity in the event of a partner’s death or retirement. However, traditional funding methods, such as term life insurance, may not provide the flexibility and long-term benefits that business owners need. Instead, utilizing a permanent life insurance policy with strategic ownership structures can offer enhanced financial advantages.

The Shortcomings of Traditional Buy-Sell Agreement Funding

Historically, BSAs have been funded using term life insurance due to its lower cost. However, this approach fails to account for the long-term financial needs of business owners. Term insurance provides only a death benefit without accumulating cash value or offering living benefits, making it an inefficient funding mechanism when viewed through a broader financial planning lens.

Many business owners also struggle with the issue of policy control. In a traditional cross-purchase agreement, one owner holds the policy on the other, creating potential ownership conflicts. Conversely, in a stock redemption plan, the business owns the policy, limiting the individual owner’s access to policy benefits. These issues often stem from a lack of awareness regarding alternative structuring options that could provide both control and financial leverage.

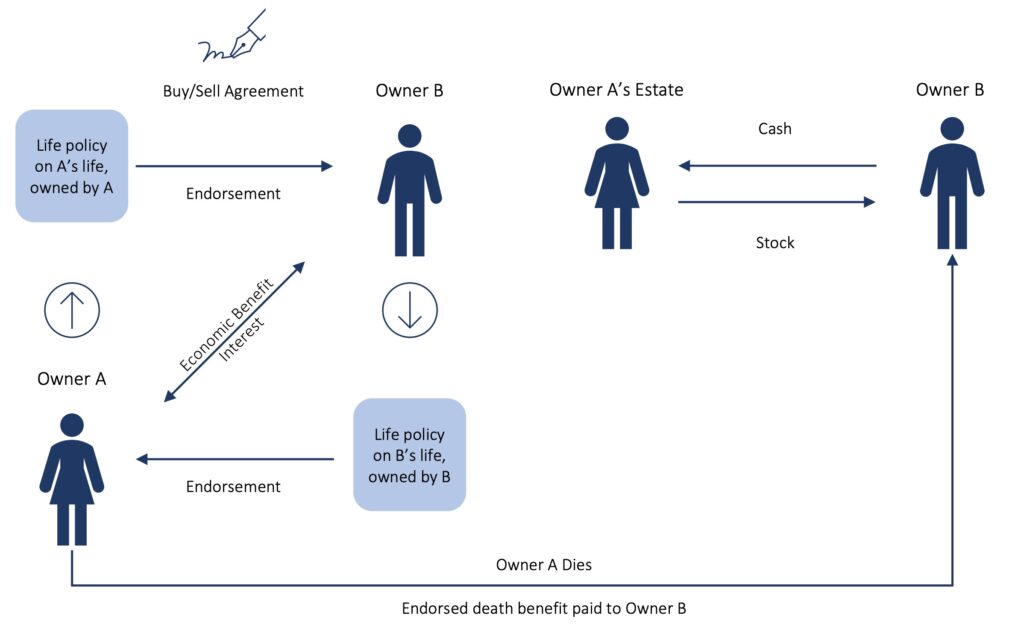

A Superior Alternative: The Cross-Endorsement Buy-Sell Agreement

To address these concerns, financial advisors should consider recommending a Cross Endorsement BSA. This structure provides business owners with control over their own policies while securing necessary buyout funds in the event of a partner’s death.

Key Features of the Cross-Endorsement Approach:

- Each business owner owns a permanent life insurance policy on their own life.

- Owners control the policy’s cash value, death benefit, and any living benefits.

- A formal assignment secures the portion of the death proceeds needed to buy out a deceased owner’s share.

- The policy remains a valuable asset for personal financial planning, including retirement income and long-term care.

- The structure avoids unnecessary taxable events or complex transfer-for-value rule complications.

Figure 1: Cross Endorsement Buy/Sell Agreement Mechanics

Maximizing Policy Utility for Business Owners

Advisors should encourage business owners to view their life insurance policies as strategic financial tools rather than mere expenses. By leveraging the benefits of permanent insurance, policies can serve multiple purposes beyond BSA funding:

- Personal Protection: Assess whether the business owner’s personal insurance needs are adequately met. If not, the coverage amount can be adjusted to accommodate both business and personal obligations.

- Long-Term Care Planning: Many permanent policies offer Chronic Illness or Long-Term Care riders, which can provide essential benefits as the owner ages.

- Retirement Planning: Cash value accumulation within a permanent policy can serve as a tax-advantaged supplement to retirement income, particularly for owners who face contribution limitations in qualified retirement plans.

Implementation Considerations and Potential Pitfalls

While the Cross Endorsement structure offers compelling advantages, it requires careful implementation to avoid potential pitfalls. Financial advisors should emphasize the following considerations:

- Ensure a Formal, Written Agreement: A properly drafted and regularly reviewed BSA is essential for maintaining clarity and avoiding disputes.

- Regular Business Valuations: The agreement should reflect updated business valuations to ensure adequate funding.

- Tax Implications: If premiums are paid through the business, they may be treated as taxable compensation to the owner. Additionally, the economic benefit of the assigned coverage may create tax liabilities.

Advantages of the Cross-Endorsement Buy-Sell Agreement

Financial advisors should highlight the following benefits when discussing this approach with business owners:

- Personal Policy Ownership: Owners name their own beneficiaries and retain control over the policy’s cash value.

- Equitable Funding: Younger and healthier owners are not burdened with funding coverage for older or less healthy partners.

- Increased Cash Value Growth: Owners can structure policies to build substantial cash value for future use.

- Portability: If the business dissolves or the owner retires, they retain the policy and its benefits.

- Creditor Protection: Depending on state laws, personally owned policies may be shielded from business creditors.

Conclusion

For financial advisors working with business owners, the Cross Endorsement Buy-Sell Agreement represents a sophisticated yet accessible planning strategy. By replacing term insurance with a permanent solution and optimizing policy ownership, advisors can help clients achieve not only a well-funded BSA but also enhanced retirement security, long-term care protection, and financial flexibility. Encouraging business owners to think beyond the immediate need for a buyout mechanism and view their insurance as a strategic asset can transform their overall financial plan, ensuring they maximize both business continuity and personal wealth accumulation.

Helping Your Clients Unlock the Full Potential of Their Buy-Sell Agreement

As an insurance advisor, you know how crucial it is to ensure that Buy-Sell Agreements (BSAs) are properly funded. However, many business owners rely on term life insurance for funding, which often falls short in providing long-term financial security.

A Cross Endorsement BSA, utilizing permanent life insurance, offers significant advantages:

Policy Control – Business owners retain control over their policy’s cash value & benefits

Tax-Advantaged Growth – The policy serves as an asset for future retirement & wealth-building

Flexibility – Provides security beyond business continuity

Helping your clients understand the value of permanent life insurance as a tool for both business and personal planning can greatly enhance their financial future.

How are you currently advising clients on BSA funding? Let’s connect and share insights!

#InsuranceAdvisors #SuccessionPlanning #BusinessContinuity #BuySellAgreement #WealthManagement #FinancialStrategy

Subject Line: A Smarter Way to Fund Buy-Sell Agreements for Your Clients

As an insurance advisor, you’re likely already guiding your clients through the complexities of Buy-Sell Agreements (BSAs). However, many business owners are still relying on term life insurance for funding, which only provides a basic death benefit and doesn’t offer long-term financial flexibility.

A Cross Endorsement BSA, funded with permanent life insurance, has the potential to:

- Provide Control – Clients retain ownership of the policy’s cash value & benefits

- Promote Tax-Advantaged Growth – Build future retirement wealth while securing the business

- Offer Flexibility – Protect both business and personal finances

This approach not only secures a well-funded BSA but can also serve as a long-term asset for your clients’ retirement and financial planning.

If you’re interested in learning more about how you can help your clients leverage permanent life insurance for their Buy-Sell Agreement, let’s schedule a quick call to discuss how you’re structuring IUL solutions for your clients!

Best,

[Your Name and Contact Information]

Insurance Beyond Protection.

CONTACT

© Brokerage Solutions. All Rights Reserved.

Securities offered through The Leaders Group, Inc., Member FINRA/SIPC, 475 Springfield Ave., Summit, NJ 07901, (303) 797-9080. Brokerage Solutions, LLC is not affiliated with The Leaders Group, Inc.